Banks start looking for borrowers in stock market

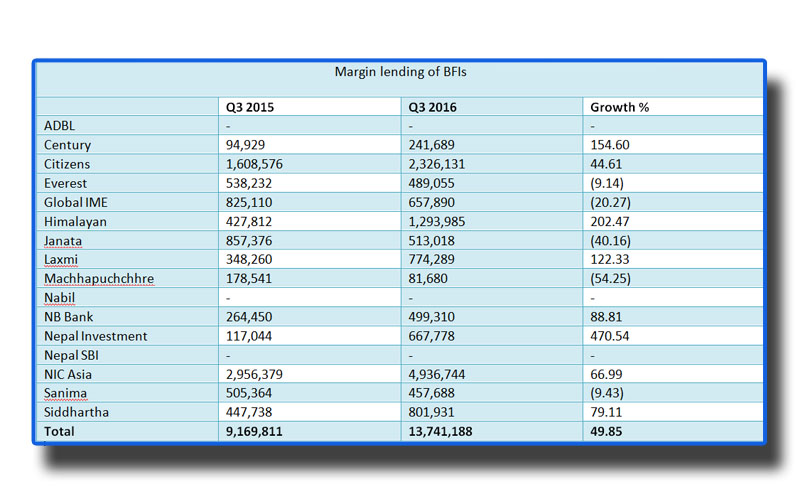

Margin lending of BFIs

Q3 2015

Q3 2016

Growth %

ADBL

-

-

-

Century

94,929

241,689

154.60

Citizens

1,608,576

2,326,131

44.61

Everest

538,232

489,055

(9.14)

Global IME

825,110

657,890

(20.27)

Himalayan

427,812

1,293,985

202.47

Janata

857,376

513,018

(40.16)

Laxmi

348,260

774,289

122.33

Machhapuchchhre

178,541

81,680

(54.25)

Nabil

-

-

-

NB Bank

264,450

499,310

88.81

Nepal Investment

117,044

667,778

470.54

Nepal SBI

-

-

-

NIC Asia

2,956,379

4,936,744

66.99

Sanima

505,364

457,688

(9.43)

Siddhartha

447,738

801,931

79.11

Total

9,169,811

13,741,188

49.85

Rs in '000; Source: Q3 Balance Sheets of Banks

Kathmandu, May 9

Text book theory that a combination of excess liquidity and lack of investment opportunities tends to divert credit towards unproductive sectors is turning out to be true in Nepal.

A sneak peek into this trend was offered by third-quarter balance sheets of commercial banks which have been made public so far.

As of today, 16 of 30 commercial banks have made their third-quarter financial statements public. These statements clearly show that commercial banks are now aggressively looking for borrowers in the stock market, as credit demand from the real sector, which slumped due to devastating earthquakes and over four-and-a-half-month-long trade embargo, is yet to pick up.

Data show a total of 16 commercial banks extended Rs 13.74 billion in margin lending, or credit issued against security of stocks, till the end of the third quarter of this fiscal year. In the same period a year ago, margin lending of these commercial banks stood at Rs 9.17 billion.

This implies loans extended on the back of stocks jumped by 50 per cent within a year.

Coincidentally, the benchmark stock index has rallied in a similar fashion. The index, which stood at 961.23 points in the beginning of this fiscal year in mid-July, today closed at 1,482.90 points, marking a surge of 54.27 per cent.

“The underlying performance and fundamentals of many listed companies do not justify the steep hike in their share prices. This means stock price hike may not sustain for a long time. This calls for prudence while issuing credit on the back of stocks,” said Sashin Joshi, CEO of Nabil Bank, the largest sector private bank in terms of asset, which had not extended loan against stocks till the end of the third quarter.

Stock market in Nepal has never been driven by fundamentals or intrinsic value of shares. For instance, economic growth rate of this fiscal year is expected to hover around 0.77 per cent, but stock investors appear highly optimistic, which, in turn, is heating the market.

All this is happening largely because of hike in flow of workers’ remittances. Nepalis working abroad sent home Rs 427.37 billion in the first eight months of the current fiscal, up 15.2 per cent than in the same period of last fiscal.

This flow of money has raised deposit levels at banks. But since there is very little demand for credit, money has started flowing into one of the few areas that is on the rise: the stock market.

Many say the current trend is not worrying because loans extended by commercial banks to stock investors stood at less than two per cent of their credit portfolio till the end of the third quarter. But others say the pace at which some of the banks are raising their exposure to the share market is worrying.

NIC Asia Bank, for instance, expanded its portion of margin lending by 66.99 per cent to Rs 4.94 billion in the third quarter. The loan issued by the bank against the back of stocks is almost 9.5 per cent of its credit portfolio of Rs 52.50 billion.

Nepal Investment Bank Ltd, too, raised its exposure to the stock market by a whopping 470.54 per cent in the third quarter. But the credit it has extended to stock investors stands at Rs 667.78 million, which is less than a per cent of its credit portfolio of Rs 84.37 billion.

Another bank that saw significant jump in margin lending is Himalayan. It saw 202.47 per cent hike in its margin lending to Rs 1.29 billion in the third quarter. This loan amount, however, is less than two per cent of its credit portfolio of Rs 65.29 billion.

“I assume banks are not recklessly increasing their margin lending. But if they are they should be careful, as they might get hit once the downturn begins,” Joshi said.